Cash Flow Statement: Learn to Develop Cash Flow Statement Template in Excel

Learning to develop cash flow statement template becomes quite easy if you have the basic information of what is cash flow statement, its structuring and basic analysis. Thus in order to make you aware of how to develop templates for cash flow statement I will begin with a small introduction to cash flow statement and its analysis.

Click to Download Cash Flow Statement Template for LinkedIn

INTRODUCTION TO CASH FLOW STATEMENTS

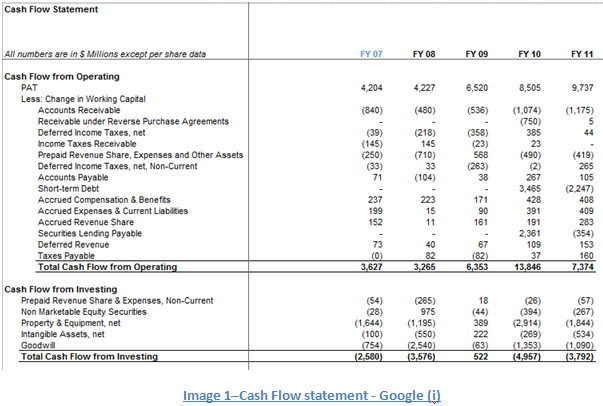

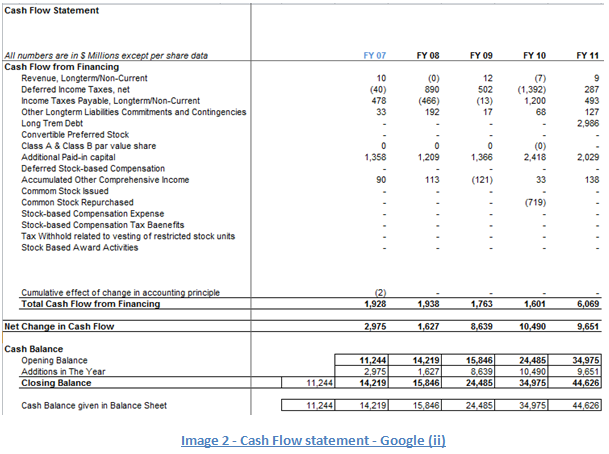

Cash Flow statements report company’s cash receipts & payments over a particular period of time. It provides information that the Income statement can’t provide as the income statement is based on accrual accounting and not cash accounting. It includes all the matters affecting the cash and its equivalents and excludes all the transactions not relating to cash. Also get a complete idea of what this means by referring to Image 1 and Image2 that show the analysis of “Cash Flow Statement of GOOGLE”.

Cash flow statements turn out to be one of the most valuable financial statements that help assessing the company’s present financial status, its capabilities and financial strength. Various important facts that are produced by statements of cash flow are listed below:-

· Report on company’s cash receipts & payments over a particular period

· Report on company’s operating, investing and financing activities

· Help to understand the effect of accrual accounting entry on cash flows

Click to Download Cash Flow Statement Template for LinkedIn

INTRODUCTION TO CASH FLOW STATEMENTS

Cash Flow statements report company’s cash receipts & payments over a particular period of time. It provides information that the Income statement can’t provide as the income statement is based on accrual accounting and not cash accounting. It includes all the matters affecting the cash and its equivalents and excludes all the transactions not relating to cash. Also get a complete idea of what this means by referring to Image 1 and Image2 that show the analysis of “Cash Flow Statement of GOOGLE”.

Cash flow statements turn out to be one of the most valuable financial statements that help assessing the company’s present financial status, its capabilities and financial strength. Various important facts that are produced by statements of cash flow are listed below:-

· Report on company’s cash receipts & payments over a particular period

· Report on company’s operating, investing and financing activities

· Help to understand the effect of accrual accounting entry on cash flows

Further what is required is the “Cash Flow Analysis”. Cash flow analysis is helpful to analysts as they provide information on whether:-

· Regular operations are generating enough cash to sustain the business

· Enough cash is being generated to pay off existing debts as they mature

· The firm has the capacity to acquire new business opportunities in future

· The firm needs additional financing

· Unforeseen obligations can be met

Cash Flow Analysis – An introduction

Realising the essence of cash flow statements and cash flow analysis let me begin with basic fundamentals and ingredients to cash flow analysis.

“Cash” is a real asset. It is the most important financial component for any company. In short, Cash flow analysis tells us how and where a company spends its money (cash outflows) and how and where the money comes from (cash inflows). Constituting template for cash flow involves structuring your template around the inflows and the outflows.

An increase in asset is a cash outflow, and a decrease in asset is a cash inflow. Similarly, an increase in liability is a cash inflow, and a decrease in liability is a cash outflow.

Cash flows can be classified into:

· Operating Cash flows: generated from normal business activity

· Investing Cash flows: generated from investments in other firms & acquisitions etc.

· Financing Cash flows: generated from financial matters like dividend paid to stockholders, interest paid

After classification it is important to interpret the free cash flows and the performance and coverage ratios.

Cash Flow Analysis– Direct and indirect method of presenting cash from operating cash flow

Operating cash flows in a cash flow statement can be represented either using the direct method or using the indirect method.

Direct Method

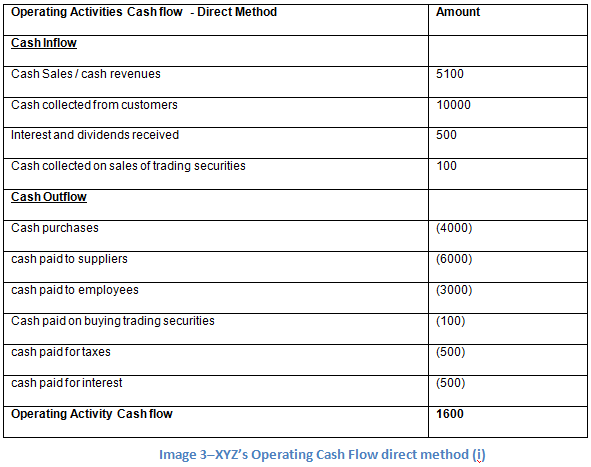

Each accrual based item on the income statement is converted into cash payments. We start with cash inflow (majorly from customers) and then deduct the cash outflows from purchases, interests, operations, and taxes. The basic philosophy here is to remove the impact of accruals and show only cash receipts and payments in statements for cash flow. The direct method for some arbitrary company XYZ is shown in Image 3.

IFRS and US GAAP both encourage firms to use the direct method, but sadly most of the firms use the indirect method.

Indirect Method

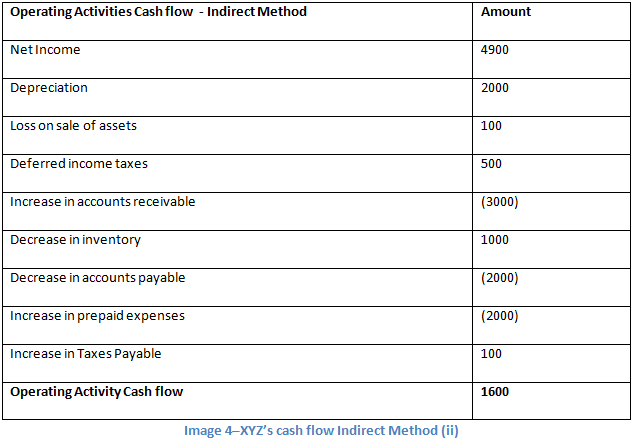

The indirect method doesn’t require specific cash transactions as also shown in Image 4. Here, we adjust the net income to calculate the operating cash flow. Adjustments are done for:

· Financing or investing activity cash flow

· Non cash items

· Changes in working capital

· Regular operations are generating enough cash to sustain the business

· Enough cash is being generated to pay off existing debts as they mature

· The firm has the capacity to acquire new business opportunities in future

· The firm needs additional financing

· Unforeseen obligations can be met

Cash Flow Analysis – An introduction

Realising the essence of cash flow statements and cash flow analysis let me begin with basic fundamentals and ingredients to cash flow analysis.

“Cash” is a real asset. It is the most important financial component for any company. In short, Cash flow analysis tells us how and where a company spends its money (cash outflows) and how and where the money comes from (cash inflows). Constituting template for cash flow involves structuring your template around the inflows and the outflows.

An increase in asset is a cash outflow, and a decrease in asset is a cash inflow. Similarly, an increase in liability is a cash inflow, and a decrease in liability is a cash outflow.

Cash flows can be classified into:

· Operating Cash flows: generated from normal business activity

· Investing Cash flows: generated from investments in other firms & acquisitions etc.

· Financing Cash flows: generated from financial matters like dividend paid to stockholders, interest paid

After classification it is important to interpret the free cash flows and the performance and coverage ratios.

Cash Flow Analysis– Direct and indirect method of presenting cash from operating cash flow

Operating cash flows in a cash flow statement can be represented either using the direct method or using the indirect method.

Direct Method

Each accrual based item on the income statement is converted into cash payments. We start with cash inflow (majorly from customers) and then deduct the cash outflows from purchases, interests, operations, and taxes. The basic philosophy here is to remove the impact of accruals and show only cash receipts and payments in statements for cash flow. The direct method for some arbitrary company XYZ is shown in Image 3.

IFRS and US GAAP both encourage firms to use the direct method, but sadly most of the firms use the indirect method.

Indirect Method

The indirect method doesn’t require specific cash transactions as also shown in Image 4. Here, we adjust the net income to calculate the operating cash flow. Adjustments are done for:

· Financing or investing activity cash flow

· Non cash items

· Changes in working capital

A thing to note while maintaining cash flow statements is that in the direct method, the starting point is ‘revenues’, the top line of the income statement. Whereas, in the indirect method, the starting point is the bottom line of the income statement ‘net income’.

However, the total operating cash flow will always be same, regardless of whether the direct or the indirect method.

Generating the cash flow statement of a company as mentioned above firstly involves the cash flow analysis for it. Given below are several important points that you should know if you want to perform a cash flow analysis of any company

Negative operating cash flow –

In general, a negative operating cash flow is a question mark on sustainability of business

In early stage of growth, a firm may have negative operating cash flow, which it finances externally through debts and equity securities. But in the long run, these sources are not sustainable and eventually every firm has to generate positive operating cash flow entries in the cash flow statement.

Comparison of earnings with operating cash flows –

· Operating cash shows gives an indication on the quality of firm’s earnings

· In general, a stable relationship points to better quality earnings

· If there is low cash flow compared to earnings, it point to(over) aggressive revenue recognition policies

Selling assets to generate cash flow from investing activity –

· A firm may sell its asset to show generation of cash in the cash flow statement but this will lead to a higher cash outflow in the future

· Size, trends – if huge can be a question mark on future

Investing / financing activity can show uses of debt:

· Debt should be used in productive activities

· Not in paying dividends or acquiring stocks

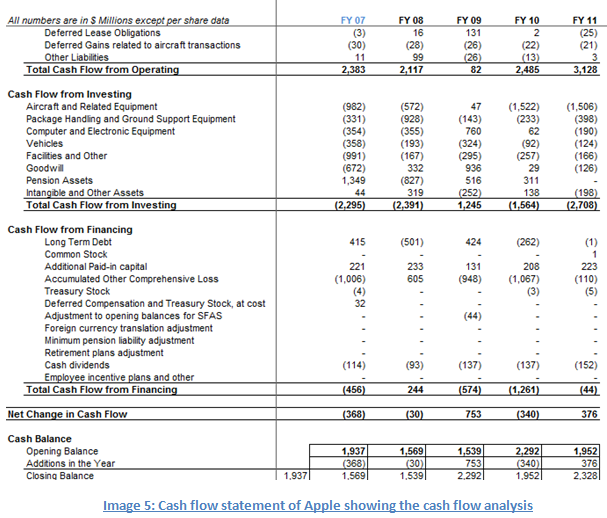

Shown below is a cash flow analysis statement of Apple. We can see that even though cash flow from financing is negative, the cash flow from operating activities is positive and increasing in recent years.

However, the total operating cash flow will always be same, regardless of whether the direct or the indirect method.

Generating the cash flow statement of a company as mentioned above firstly involves the cash flow analysis for it. Given below are several important points that you should know if you want to perform a cash flow analysis of any company

Negative operating cash flow –

In general, a negative operating cash flow is a question mark on sustainability of business

In early stage of growth, a firm may have negative operating cash flow, which it finances externally through debts and equity securities. But in the long run, these sources are not sustainable and eventually every firm has to generate positive operating cash flow entries in the cash flow statement.

Comparison of earnings with operating cash flows –

· Operating cash shows gives an indication on the quality of firm’s earnings

· In general, a stable relationship points to better quality earnings

· If there is low cash flow compared to earnings, it point to(over) aggressive revenue recognition policies

Selling assets to generate cash flow from investing activity –

· A firm may sell its asset to show generation of cash in the cash flow statement but this will lead to a higher cash outflow in the future

· Size, trends – if huge can be a question mark on future

Investing / financing activity can show uses of debt:

· Debt should be used in productive activities

· Not in paying dividends or acquiring stocks

Shown below is a cash flow analysis statement of Apple. We can see that even though cash flow from financing is negative, the cash flow from operating activities is positive and increasing in recent years.

From where can I get the Cash Flow Statement to perform cash flow analysis?

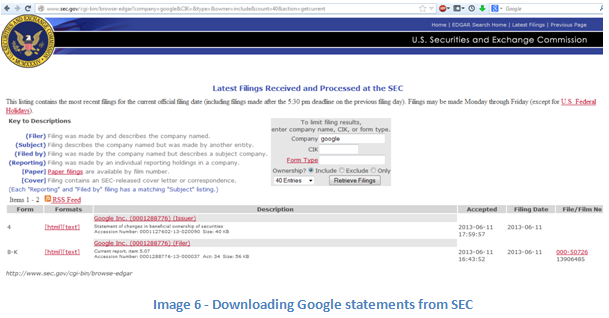

With the advent of internet and IT, financial statements like cash flow statements are getting more and more accessible to common man with every passing day. Most companies make available their quarterly and annual reports on their corporate website. In the US, all companies filing with the SEC (http://www.sec.gov/) are required to supply their documents to a service called EDGAR. EDGAR has free access to more than 20 million filings. You can also go to http://www.sec.gov/edgar/searchedgar/webusers.htm and go through a tutorial on how to use EDGAR.

Click to Download Cash Flow Statement Template for Real Life Company

With the advent of internet and IT, financial statements like cash flow statements are getting more and more accessible to common man with every passing day. Most companies make available their quarterly and annual reports on their corporate website. In the US, all companies filing with the SEC (http://www.sec.gov/) are required to supply their documents to a service called EDGAR. EDGAR has free access to more than 20 million filings. You can also go to http://www.sec.gov/edgar/searchedgar/webusers.htm and go through a tutorial on how to use EDGAR.

Click to Download Cash Flow Statement Template for Real Life Company

Key Things to Note in doing a cash flow analysis

1. Pay attention to whether the cash flow analysis classification is done under IFRS or US GAAP. There are many important differences between the two.

2. Almost always, cash flow ratio analysis is performed as a comparison analysis, which can be

a. time series - comparing current years ratio with previous years ratios

b. cross sectional – comparing the company’s ratio with the industry

3. You should know what exactly each ratio is measuring, but more importantly, you should know whether a higher ratio or a lower ratio is better

In order to learn about Profit and Loss Statement "CLICK HERE".

1. Pay attention to whether the cash flow analysis classification is done under IFRS or US GAAP. There are many important differences between the two.

2. Almost always, cash flow ratio analysis is performed as a comparison analysis, which can be

a. time series - comparing current years ratio with previous years ratios

b. cross sectional – comparing the company’s ratio with the industry

3. You should know what exactly each ratio is measuring, but more importantly, you should know whether a higher ratio or a lower ratio is better

In order to learn about Profit and Loss Statement "CLICK HERE".